Future Member Experience Trends

My takeaways talking with payer and digital tech leaders

Introduction

This fall five regional payer Chief Experience Officers and myriad founders and leaders at payer-focused start-ups indulged my requests to interview them. I wanted to know how member experience is changing and how those trends will progress.

The regional plan Chief Experience Officers (CXOs) are facing two immediate challenges.

First, they must support their organizations’ broader mandate to offer lower cost plans. Utilization is up and continues to be unstable from continued post-pandemic “make up” care and, I suspect, up-coding from the 40% of providers adopting ambient scribing agents.

The challenge for member experience teams is to proactively partner with the rest of the org to ensure that new plan designs, networking approaches, and other changes are designed with members’ experience in mind so the changes are fully effective.

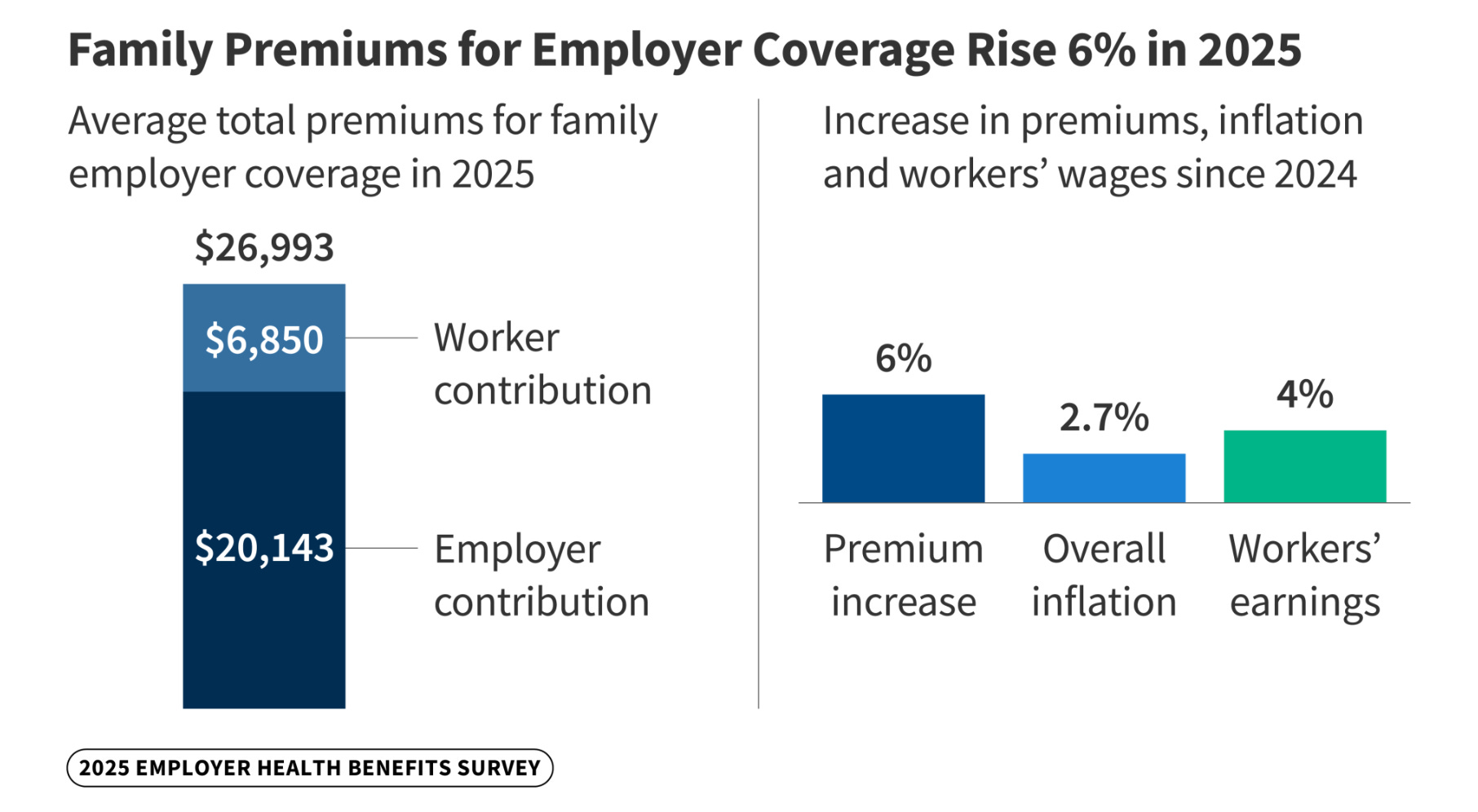

Second, they must improve member NPS. Starting with the assassination of the UHC CEO and continuing with the shutdown, the high cost of healthcare has featured prominently in the news. Because payers are typically the whipping horse of the healthcare system in broader societal discussions about cost, payer NPS scores have declined precipitously.

This presents CXOs with a challenge: how to educate members about the role of insurance and where the true costs come from without undermining relationships with providers and employers.

Yet the leaders I spoke with have a good handle on the tactics to address these two issues. Where they are not able to spend as much time: examining the nascent trends, already underway in other industries and in niche parts of the healthcare market, that could dramatically disrupt the status quo trajectory of member experience if they catch on and scale.

If one of the trends “flips” and sees widespread adoption there would be seismic impacts. The below report considers the shifts in technology, consumer preferences, and business models that, if they quickly scale up, could profoundly change members’ relationship with their payer.

The benefit of this report for you, dear reader: awareness so you can hedge against the chance these trends accelerate, look good by proactively educating your colleagues on these trends, and make savvy investments with your resources.

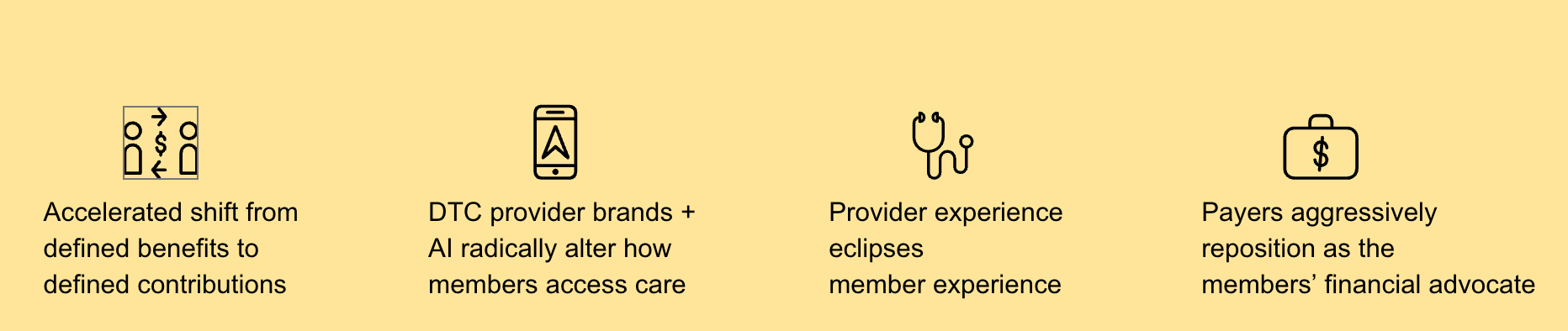

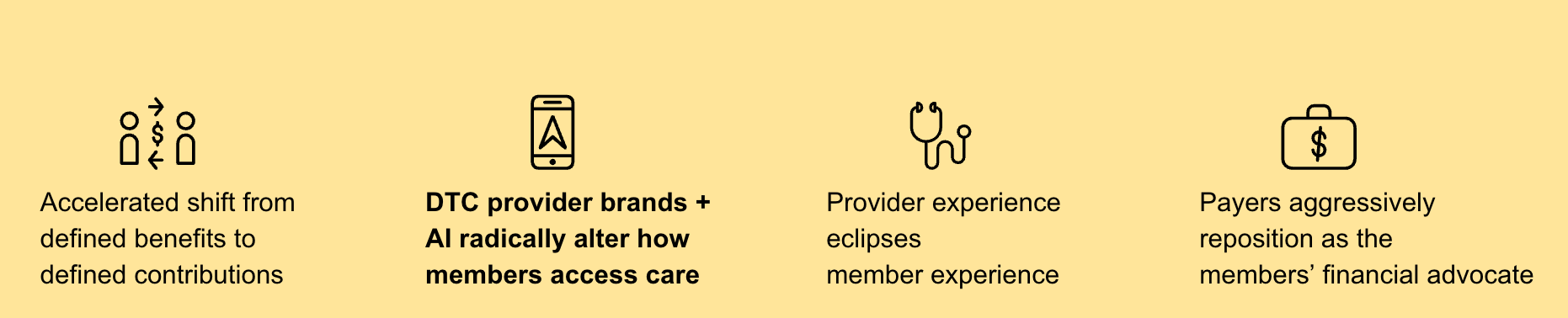

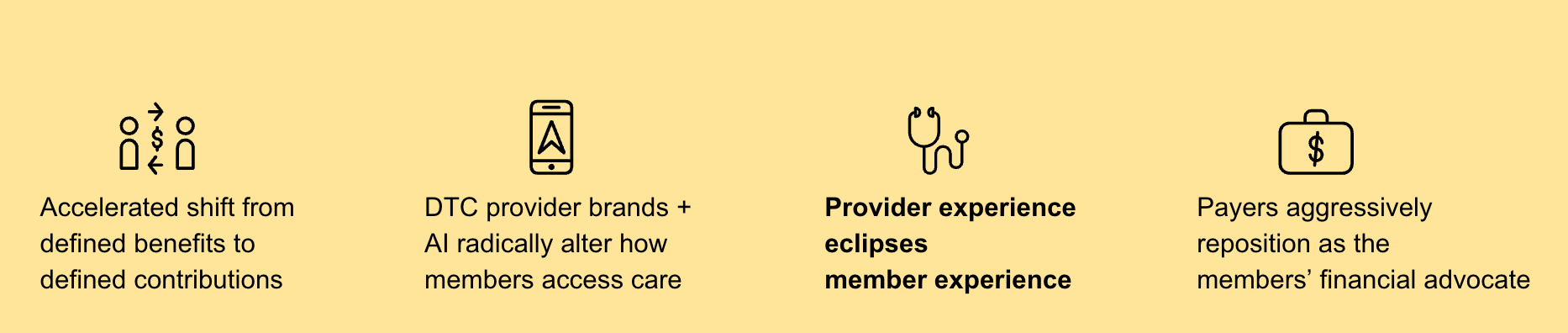

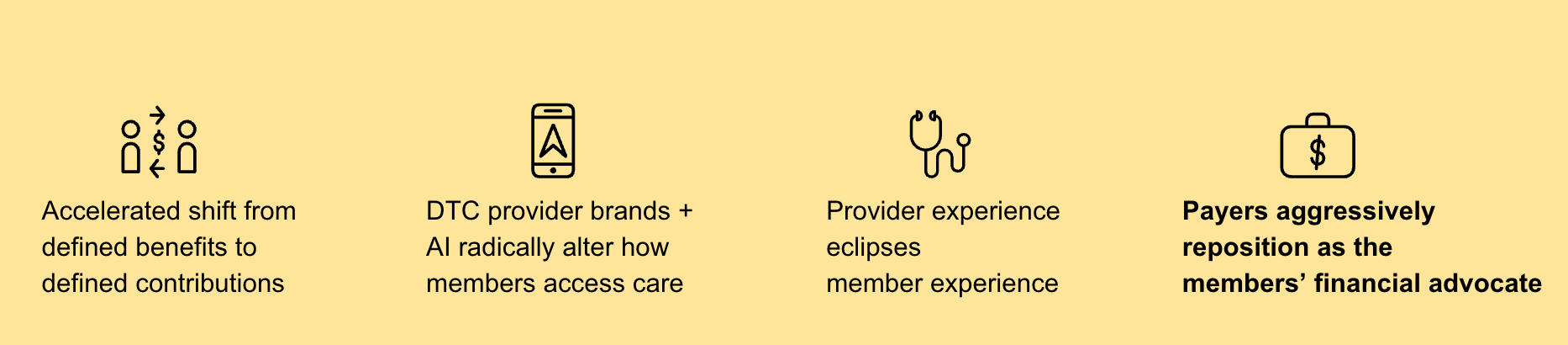

Four developing trends that could fundamentally disrupt member experience:

1 - Accelerated shift from defined benefits to defined contributions

2 - DTC provider brands and AI radically alter how members access care

3 - Provider experience eclipses member experience

4 - Payers aggressively reposition as the members’ financial advocate

Trend 1: Accelerated shift from defined benefits to defined contributions

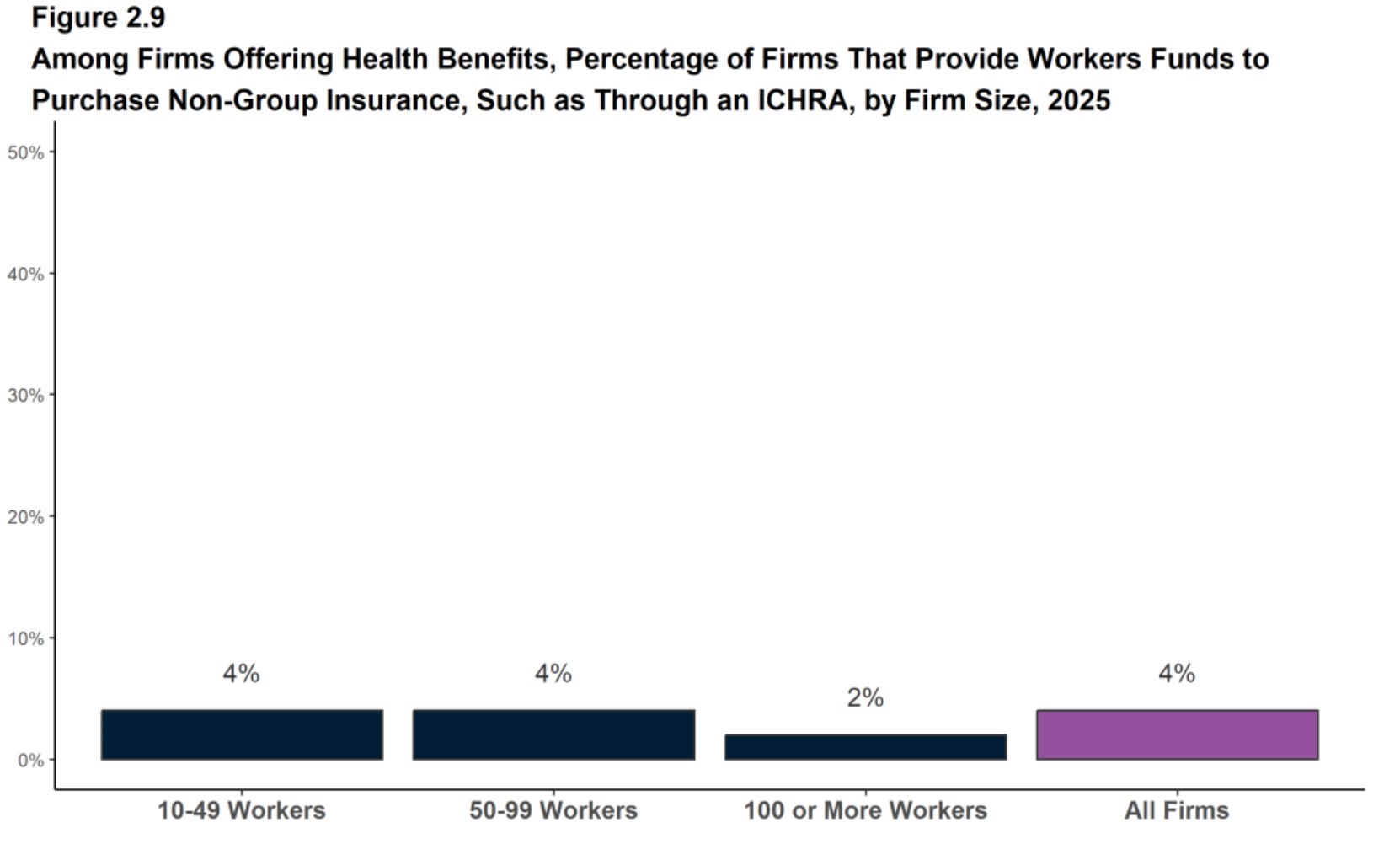

Few companies have acted upon ICHRA legislation to move away from providing defined benefits to instead provide tax-advantaged payments directly to employees for healthcare-related expenses.

There have been two major barriers:

1 - Employee recruiting and retention disruption. This would be a major shift in employee’s compensation structure and expectations; a tight labor market through the early 2020s made the move too risky.

2 - Poor ACA risk pools. The companies with younger, tech-forward employees that are open to this shift are also full of…younger, high socio-economic status, healthier employees. This means they can buy better coverage as an employer group than the individual employees could purchase on the ACA market with it’s sicker, more expensive risk pool. So the same $5K per employee contribution goes further if used in employer group plan than individually on the exchanges.

However, the shift from defined benefits to defined contributions could happen suddenly and, if it did, would dramatically change how legacy payers must design and sell plans.

There are several factors which could fundamentally accelerate the shift to defined contributions:

1 - Employers are at their breaking point with healthcare costs.

Many employers are already capping the amount they contribute to employees health insurance, putting the full cost difference for more expensive plans upon the employee.

Yet the optics of reducing the ~70% of premiums employers typically pay, further shifting expenses upon employees each year, are terrible. A complete system switch framed under the guise of better plan personalization on the IFP market for employees is potentially more workable.

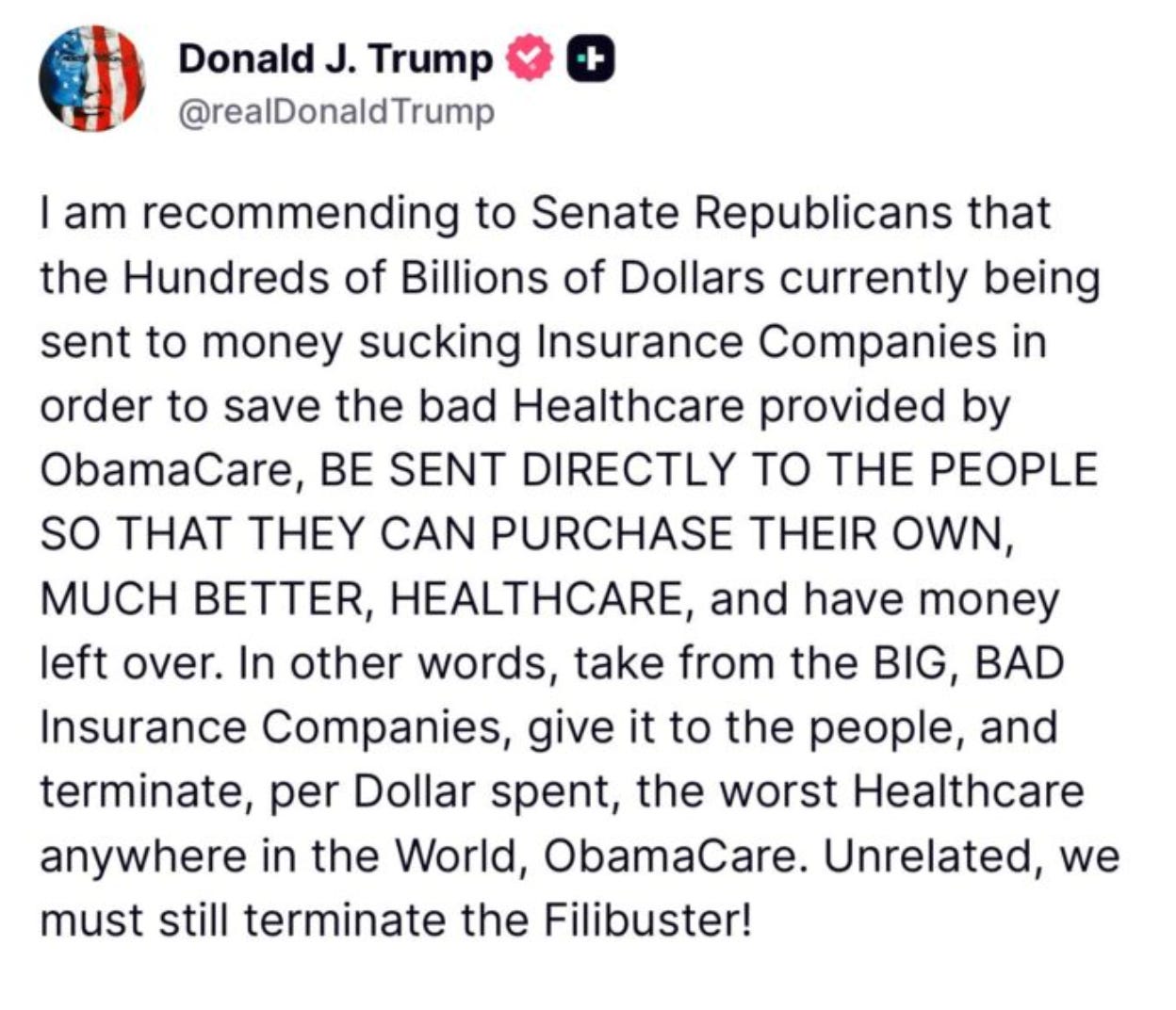

It’s worth noting that, while very unlikely to come to anything, this shift to defined contributions is also in-vogue with the republican party as the alternative to extending the ACA subsidies.

2 - The entrenchment of remote work and short employee tenures.

Remote work is here to stay. This makes it harder for HR leaders to offer at-parity benefits across the country and nudges them towards providing a defined contribution instead.

With employees switching jobs every several years, it’s a benefit to them if they move from one ICHRA employer to another and can keep their same plan from the exchanges.

3 - Personalization of benefits (and the young and healthy looking for more value from their benefits).

I suspect the switch to ICHRA will be framed as an empowering move for employees. It’s unwinding the paternalism of the company dictating the carrier and network that the entire company must use. Instead, employees can choose the carrier or plan that fits their needs.

I think this framing will be popular because it will allow the young and the healthy to get more value out of their defined contribution. Insurance, of course, is a cross-subsidy from healthy to the sick, which means also the young to the old.

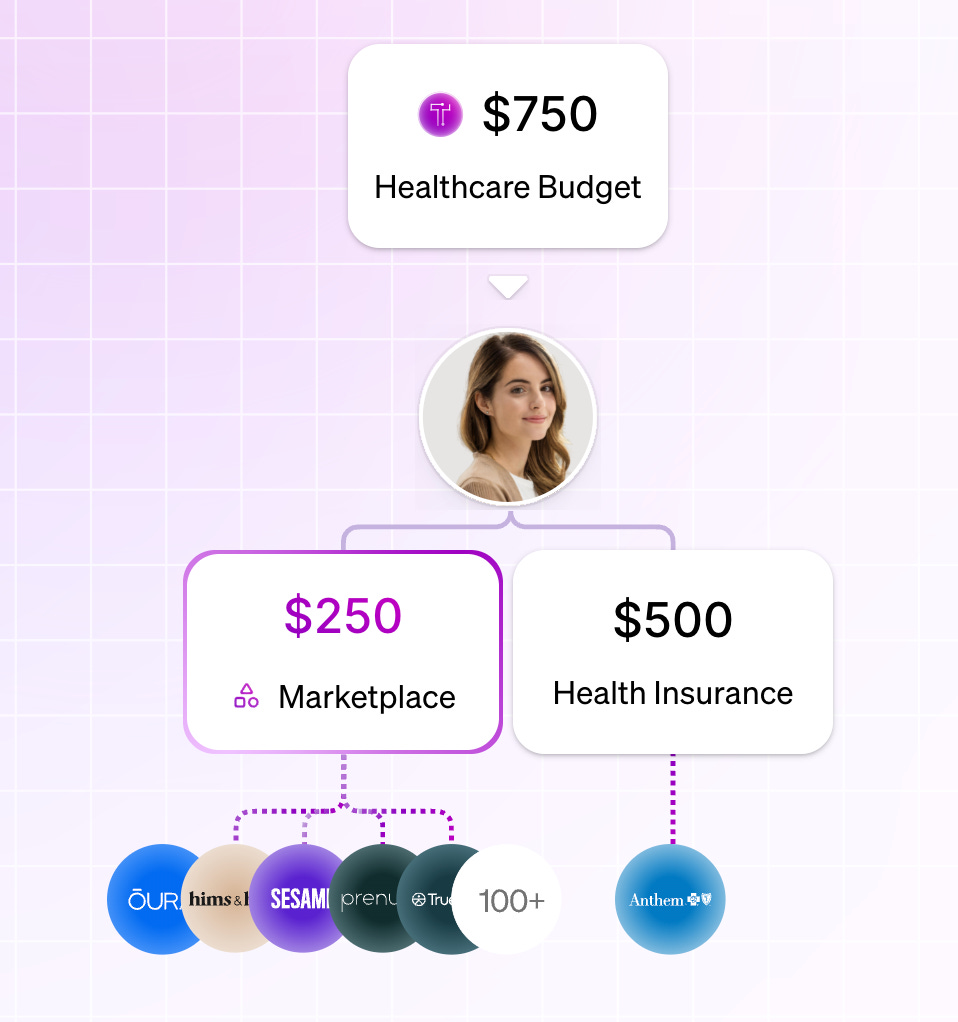

Outside of maternity benefits, younger employees currently get little value from their plans. ICHRA plans allow them to buy true catastrophe plans at a much lower premium and then spend leftover dollars directly on prescriptions, wearables, health optimization services etc.

4- ICHRA platforms make it smooth to switch (for employees and employers)

It’s a hassle for HR leaders to manage healthcare benefits; to choose between carriers, run open-enrollment, comply with all the ERISA regs, etc. There’s now a relatively mature ecosystem of ICHRA platforms like Thatch and Venteur that reduce the burden on HR; just set the budget and rules and allow platform to run the rest.

It’s also worth noting that most employees don’t realize how much their employers is putting in for their premium benefits; handing out “cash” could feel like a greater benefit.

There are two major implications for legacy payers:

A reduction in the total amount of health insurance purchased.

You’ll likely see healthy, younger, and more risk-tolerant employees opting for lower-premium catastrophe insurance in order to use the remainder of their contribution for direct purchases of DPC, provider bills, etc.

Another consequence: consumers will feel emboldened to buy health insurance using their employer contribution alone. Rather than choosing employer-sponsored plans where their contribution is pre-defined, it will feel more painful for price-sensitive employees to spend out-of-pocket on plans. They’ll likely just seek to buy lower-coverage insurance using the contribution alone.

A threat of new platforms stepping into the role traditionally provided by payers.

Health insurance companies are the de-facto two-sided healthcare platform connecting those that need care with care providers. They bring both sides to the platform and set the marketplace rules. This is true both for employers purchasing insurance and members utilizing insurance.

However the shift to defined benefits will create demand for a “marketplace” of health services beyond traditional insurance. Both the big consultants (Aon, Mercer, etc.) and new ICHRA platforms like Thatch could step into this role if and build out the marketplaces faster than traditional carriers.

Strategies for payers to consider:

Business model innovation.

Payers will have to accelerate their efforts hold premiums steady for remaining customers and avoid a death spiral. This includes efforts to reimagine plans around DPC, narrow networks, reference-based pricing, etc.

Just as the shift from Fully Insured to ASO products forced payers to adapt with new business models and services (low fee for the basic ASO program, upsell accessory services), the shift to ICHRA will force payers to identify new service bundles that appeal to consumers directly and re-capture the revenue from employer-sponsored benefits.

For instance, you could imagine a plan that is marketed and built around peri-menopausal women. Included int he plan design: access to Midi Health, partnerships with other brand affiliates.

This would also serve to bundle in attractive services with the traditional insurance people still need, and by appealing to specific demographics, re-create some of the risk-pool advantages that employees of select companies enjoy now.

DTC marketing, purchasing, and experience.

This will be a radical change for payers and will elevate and evolve the role of Chief Experience Office. Payers will need to better understand each member segment and how to appeal to them, from co-branding efforts to influencer strategy. “Enrollment” will be replaced by a more modern purchasing flow, and member service will take on a bigger role in the organization to uphold the brand.

Payers will need to become more sophisticated in leveraging their current data on members to design products that they know will appeal.

Trend 2: DTC provider brands and AI radically alter how members access care

The default model of accessing care through one’s PCP has weakened in the past 20 years. Broad PPO networks and provider review sites like ZocDoc allowed members to book directly with specialists. Urgent Care replaced the PCP for low-acuity medical emergencies while online telehealth services allowed patients to get prescriptions for low-acuity. Patients turned to WebMD to self-diagnose.

Still, for more serious issues or where the patient is unsure what the concern was, the PCP remains the point of entry to care. Health systems’ spending spree in the 2010s purchasing independent PCP medical groups was largely to capture that patient acquisition funnel and redirect referrals within the health system.

But AI could accelerate the consumerization of healthcare. As WebMD traffic plummets and patients turn to AI to navigate the health system, companies like Doctronic.ai are putting a skin on LLMs to convert patients to cash-pay telehealth visits. More interestingly, Verily recently launched their own medically trained LLM that will aggregate data from both health systems and wearables to provide initial diagnoses. It’s not hard to imagine prestige health systems like Mayo taking a similar approach and then directing patients to schedule an appointment.

Update on 12.16: General Intelligence, a digitally native practice focusing on low-acuity healthcare services started by the founders of PillPack, also just pushed out this exact same model. Use AI to gather all context on a patients’ medical history, then use the chatbot to steer the patient to the appropriate service.

AI will also likely continue to normalize D2C access of medication. The rise of GLP-1s has popularized an approach to medicine that used to be centered around the sexual health market with companies like HIMS and RO. AI will likely continue to facilitate this, making it easier for companies to identify the medication members are seeking and the make the case that it’s medically necessary.

This is on top of a closely related trend of medical brands replacing individual PCPs. Midi Health is an interesting case study here; rather than a woman’s conversation with her PCP or even OBGYN evolving as she enters middle age, women are signing up directly with Midi Health to address a specific health need.

There could be benefits to all of this for payers. These services have a bias for cash pay (it’s part of the convenience play), and it’s not hard to imagine fewer low-cost claims. Yet there are also risks the payers to guard against and adapt to:

Making cash pay easy and convenient further degrades the need for insurance among the relatively healthy that currently subsidize the sick and keep premium payments lower. There’s a risk that this trend pairs with the shift to defined contributions to lower the total spend that filters through payers

It could also lead to more claims. While some may deride the PCP-centric model as paternalistic and celebrate more unfettered access to medications, most PCPs are wary of overprescribing medications and that provides payers with a natural friction to additional claims for medication.

Perhaps the biggest threat, though, is that provider-led LLMs will undermine payers’ efforts to navigate members to the best performing, lowest total cost of care providers. Payers are investing in navigation plays like Carrum health and Garner that stand up Centers of Excellence and incentives and guide patients to them. Yet these efforts could be undercut if providers are quicker to adopt a the LLM-based navigation that patients are eager to use.

Further reading: https://www.healthcare-brew.com/stories/2026/02/09/health-systems-competing-ai-search-tools-patients?mc_cid=7d39aa7ad8&mc_eid=8bd8252954

Trend 3: Provider experience eclipses member experience

Payer efforts to create well-informed members who savvily shop for healthcare services have had mixed results. Most members will always struggle to navigate complex financial and network arrangements; they’ll also always have a bias to trust their doctor and follow their suggested prescriptions, procedures, and referrals.

So payers are beginning to invest in provider experience as a way to impact member decision making and experience. Some examples: arming providers with real-time insight into plan design and coverage, pre-adjudicating procedures (CMS-0057-F is a push in this direction), and allowing providers to see how much prescribed medications may cost the member and which referrals specifically are in-network. The goal is to allow the provider, who has a better sense of alternative treatments, to consider the financial impact upon the member.

Tactical examples of this shift:

1 - Enabling providers with real-time info on plan design, utilization, and pre-adjudication.

RCM is an antagonistic process. Health systems have eagerly invested in ambient scribes to augment their RCM teams’ efforts to ensure that each visits gets the maximum allowable reimbursement. There’s a real information asymmetry here for the payers, who want to ensure care is medically necessary. (Russell Pekala, cofounder of YUZU, wrote the most interesting description of this dynamic that I’ve seen here.)

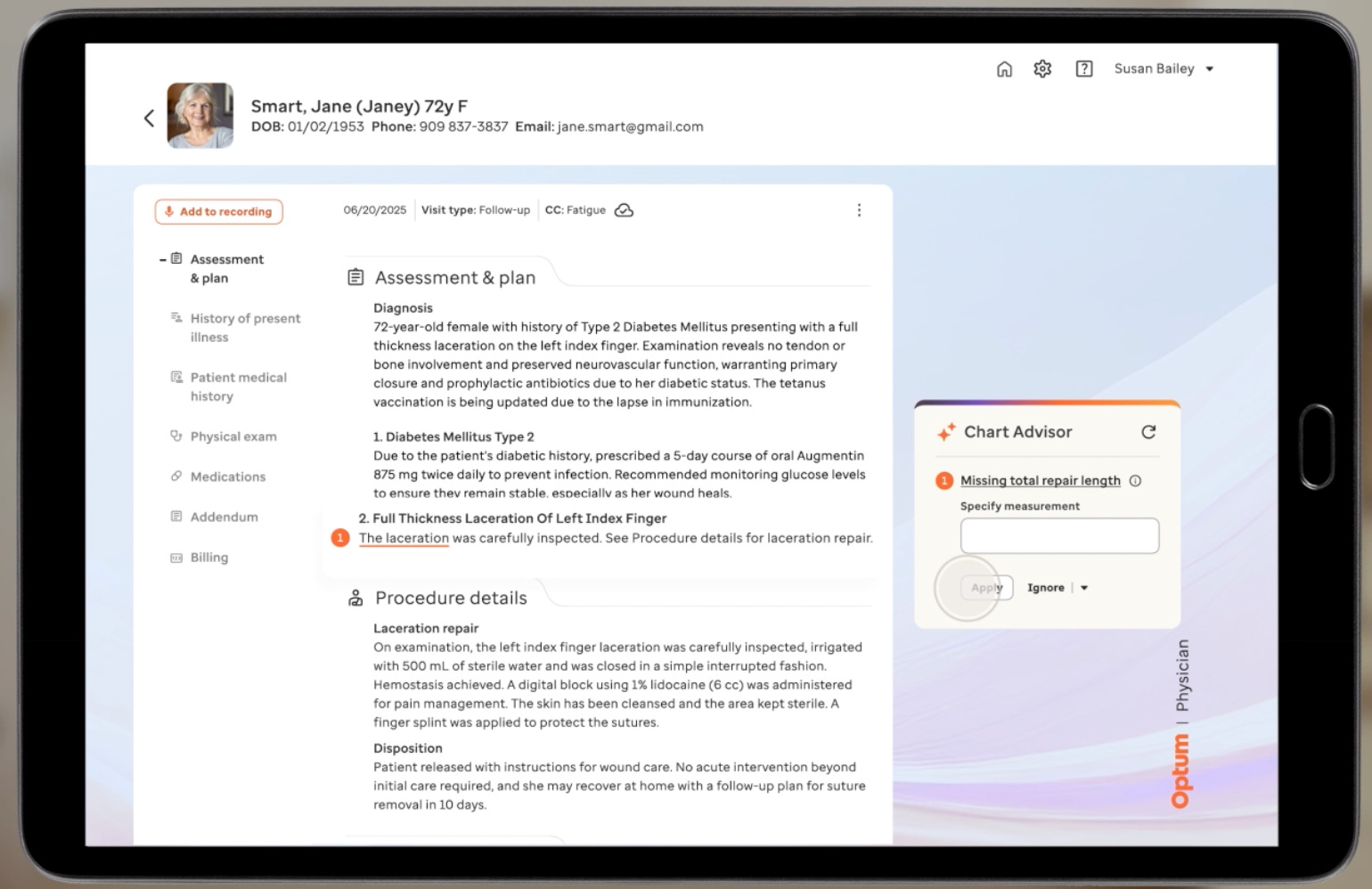

This is where Optum’s REAL product comes in. As a ambient scribe service for providers, it uses helps providers properly document encounters but also inquire real-time about coverage for procedures, care plans, etc.

I suspect United is trying to front-run the health system sponsored ambient scribes (nuance, abridge, etc.) and get providers to use their ambient scribe instead. It’s plausible that this could work, particularly with the long-tail of provider practices outside of health systems.

After all, the payer knows the rules of what documentation and coding it will accept, and their sponsored. And it will be genuinely helpful for the individual clinician who wants to help their patients with financial realities.

Of course, the value for the payer here is great. They can influence coding to ensure there’s not excessive upcoding, obtain a transcript of the call to verify calls, and have a platform upon which to help the provider steer the member twoards the desired medication, referral, care plan, etc.

2 - DCP Plans and COE plays building for provider experience

DPC plans are another example where we are already seeing far closer provider-payer collaboration. In many ways, these plans are a modern upgrade of the HMO plans of the 90s, except rather a “stick” requiring PCP referrals for specialists, plan design incentivizes patients to utilize their dedicated PCP rather than a cadre of specialists.

DCP plans are investing in their provider experience to help those providers make smarter care plan decisions for their members. For example, Jeff Yuan, a co-founder of Mending, a DPC-centered plan in the IFP markets in Maine and Oklahoma, told me that members carry the experience and care they get from their DPC provider, as part of their Mending DPC plan, into how they view the Mending brand.

In this environment, it makes sense to invest in provider experience, arming providers with the tools to quickly check which medications are covered, which specialists are in-network, quality of specialists, etc.

Plans with networks built around COEs have a similar dynamic. Beyond creating a financial relationship with top doctors to steer volume their way in exchange for discounted FFS reimbursements or value-based bundled payments, they also boost the provider experience by:

Waiving any prior auths

Waiving detailed clinical documentation and paying providers within 7 days

Augmenting their workflows. For example, Carrum Health helps members with scheduling, gathering medical documentation, and completing required paperwork to ensure their procedures with COEs are successful and not delayed.

3 - The rise of narrow networks and how it naturally favors payviders’ provider experience

Narrow networks have been fairly anemic in the commercial market, and that’s because there’s significant employee abrasion shifting to a narrow-network, provider based plan: many employees will have to switch their providers and will grumble.

However that could change rapidly, for two reasons:

First, demand for narrow networks may increase.

A post-ICHRA, defined contributions environment would side-step the barriers to narrow networks. There’s no longer a group coordination / abrastion issue from HR departments choosing a single carrier. Instead individuals can opt to make the switch to a narrow network and switch providers. And individuals who are purchasing insurance directly are more likely to consider the price between plans as they weight switching providers.

This could create a virtuous cycle for narrow networks: it’s likely that healthier members without deep existing relationships with providers are more likely to switch to the less expensive, narrow network.

Yet even without the shift to defined benefits, employers may finally be willing to risk employee friction and adopt health system based narrow networks, or at least start offering those plans. As Christina Farr wrote, the pain of rising premiums for employers is high enough that they are willing to try novel approaches despite some employee pushback. And the salient point is that, unlike most of the past decade, there is slack in the labor market and employers can prioritize cost cutting over employee experience.

Second, we could see the supply of narrow networks increase.

As health systems recognize the potential financial opportunity to become a carrier, the technology enablement layer to do so has never been better. TPA platforms like YUZU reduce the barrier to entry for health systems to spin up their own narrow plans. It has a new, clean tech stack and has natively build many of the features that employers look: variable copays, tiered networks, cash reference based pricing and cash pay options, etc

So while provider plans typically target health system employees rather than seeing widespread adoption in the commercial space, I suspect we will see a rise in health systems launching plans built around their networks. And this could give them a jump start on deeper payer-provider integration. There is already a degree of data connectivity and incentive alignment between the payer and provider sides of the business. Indeed, Kaiser’s new “Moving All to One” ad campaign explicitly touts how your doctor, pharmacy and insurance work together. While the reality of the connectivity isn’t that mature yet, the appeal could help attract members away from traditional insurance plans.

Trend 4: Payers aggressively reposition as the members’ financial advocate

Member NPS is tanking across the board, and payers are often the whipping horse of the healthcare system in the broader societal discussion about costs. But there’s an opportunity for payers to win member trust and place the PR burden on providers by more aggressively helping members avoid surprise bills and set cost expectations upfront.

Providers have largely skirted their financial responsibility to patients; the clinical decision making process is completely disconnected from the financial impact upon the patient. Providers focus on on access and clinical care, only begrudgingly proving good-faith discussions when legislation requires it. They then place blame on payers when patients are shocked at the surprise bill* they receive (”you’ll have to call your insurance company and talk to them). You may recall that in 2018 I started a price transparency company for providers that had no product-market fit b/c it wasn’t in providers’ financial interest to share upfront costs (you can read about that here)

As members continue to struggle to afford healthcare services within their deductible, there’s an opportunity for payers to position themselves as the financial protector of their members.

Tactical examples of this shift:

Front-run providers on prior cost transparency.

Prior auth give us a good illustration of what this could look like. In the current system, providers lock members’ expectations onto a suggested care path only to explain later that a different, presumably inferior care path is necessary because the health insurance plan denied the preferred course.

Instead, plans could proactively communicate prior auth processes to patients, explaining to the member directly why a physician-suggested procedure isn’t covered: “This is a major procedure that carries big risks, will be expensive for you, and may not be as effective as other, less invasive care plans that will cost less.”

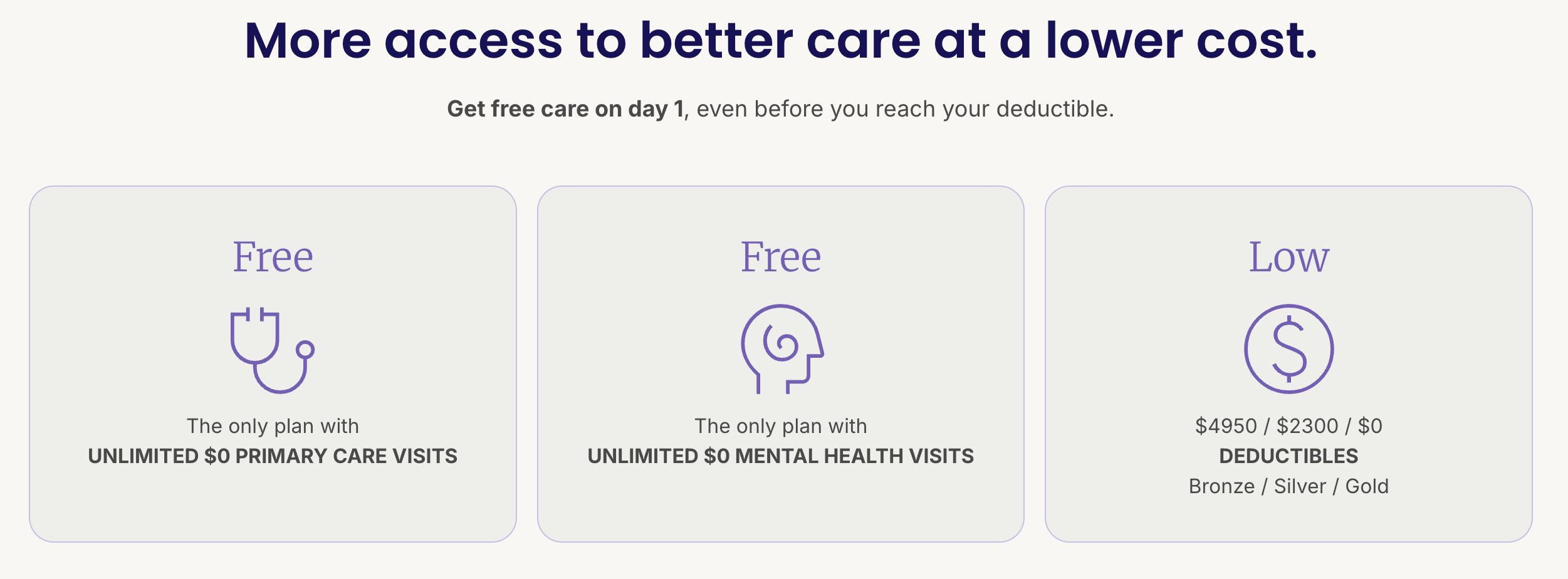

Another example of this: the more sophisticated price transparency approaches of companies like Garner and Optum’s Surest health. Rather than providing cost “estimates” these approaches waive deductibles or offer upfront, variable copays to steer members to higher quality / lower price providers. Cigna’s new tiered copay plan Clearity is another example of this approach.

Shifting the “denial” burden back onto providers.

Both reference based pricing and cash pay plans take this approach. With reference based pricing, the member and provider know upfront how much the plan will pay. If a provider won’t accept 140% of medicare, the burden is on them to explain this to the member. (A Sana Health executive told me that when they , they stipulate that cashing the check means the provider can’t balance bill the provider.)

A bit more speculative, but I spoke with a TPA platform that questioned why commercial health plans don’t take Medicare’s approach: prior auths rarely required but the reimbursements are lower. Instead of an outright denial of care, you can imagine a health plan taking the posture of:

“You can go ahead with the procedure and as a plan we will pay for 125% of Medicare’s rates for this to the provider (and the provider can’t balance bill you for the rest of what they think they should get).” Put it on the provider to then decline that procedure if they don’t think it’s worth their time and explain that to the member.

Safeguarding members from provider billing errors.

Fairly frequently, provider billing errors and upcoding efforts land on members with high-deductible plans. Payers generally provide little support helping members fight back. With my knowledge of healthcare billing I’ve identified numerous provider billing errors in my family’s bills, yet typically payers put me in the position or relaying information back and forth between the provider and them. I’d ask the insurance company “can you just take care of this for me?” but they’d say they can’t reach out to the provider directly.

There’s a big opportunity for payers to more aggressively market themselves as the protector of their members from unscrupulous billing practices. UHC does this and it’s delightful. This is anecdotal, but each time I’ve identified a provider billing issue, the United member experience associate I chat with takes down the provider info and reaches out to them directly on what codes to resubmit.

I built a prototype for a google demo day competition of how payers could more systematically provide reassurance to patients that they are not overpaying provider bills here.

Coda

Each of these trends will elevate the importance of member experience teams and leadership. Too often I’ve seen member experience teams relegated to primarily running the member experience call center. Yet just as efforts to reduce premiums won’t be successful if member journeys are not redesigned accordingly, the plans that run towards a member-first approach, and through interviews and data on maintain a close understanding of what members want, will better weather these trends.